Baton Rouge Flood Insurance Guide for Out-of-State Buyers

What Out-of-State Buyers Need to Know About Flood Insurance Before Moving to Baton Rouge

What Out-of-State Buyers Need to Know About Flood Insurance Before Moving to Baton Rouge

If you're moving to Baton Rouge from out of state, welcome, you're going to love it here. The food, the football, the front-porch friendliness, and a cost of living that stretches your housing dollar a lot further than it did back home. But there's one local topic that catches almost every newcomer off guard, and it has nothing to do with traffic on I-10 or where to find good boudin. It's flood insurance.

Here in South Louisiana, flood insurance isn't an afterthought or a box you check at closing. It's part of how we think about owning a home, and the rules around it work differently than they do almost anywhere else you might be coming from. As a born-and-raised Baton Rouge native who specializes in helping people relocate here, I want to walk you through what you actually need to know: the stuff that doesn't show up in a quick online search, and the timing traps that can cost newcomers real money.

And the timing matters more than you'd think. Just last week, in mid-June 2026, the remnants of Tropical Storm Arthur, the first named storm of the season, stalled over Louisiana and dropped historic rain. A spot in Avoyelles Parish, not far northwest of here, recorded more than 29 inches in under 12 hours, shattering the state's all-time 24-hour rainfall record. The Baton Rouge area was largely spared the worst this time, but schools closed across East Baton Rouge, Livingston, Ascension, and West Baton Rouge parishes, sandbags went out, and rivers around the metro climbed fast. It was a June reminder of something locals already know: in Louisiana, water doesn't wait for a hurricane, and it doesn't care what your flood zone map says.

The One Deadline That Catches Newcomers: Buy Before a Named Storm Is in the Gulf

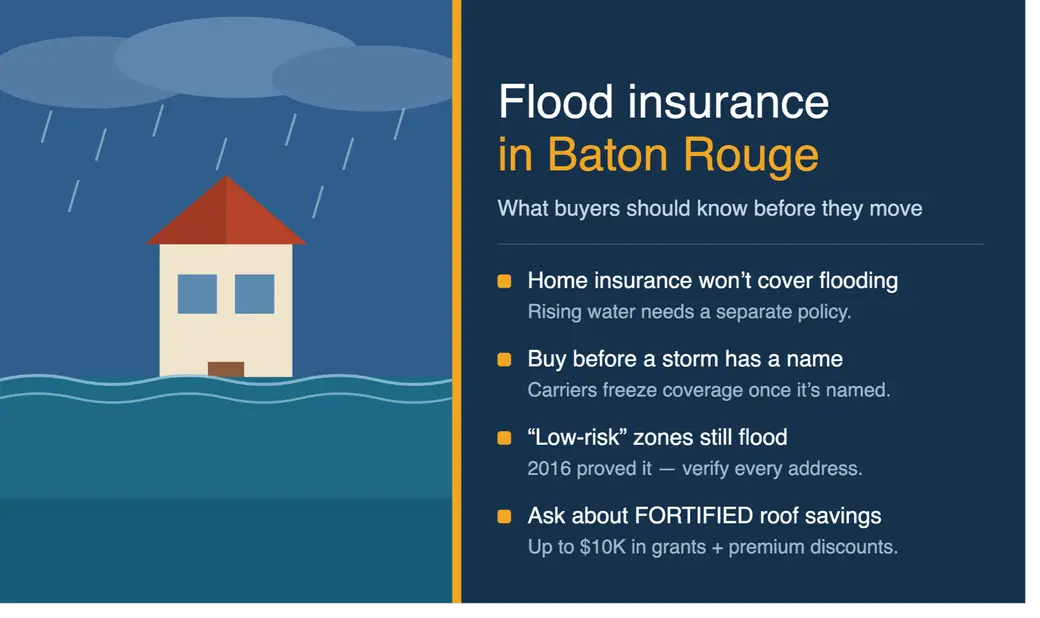

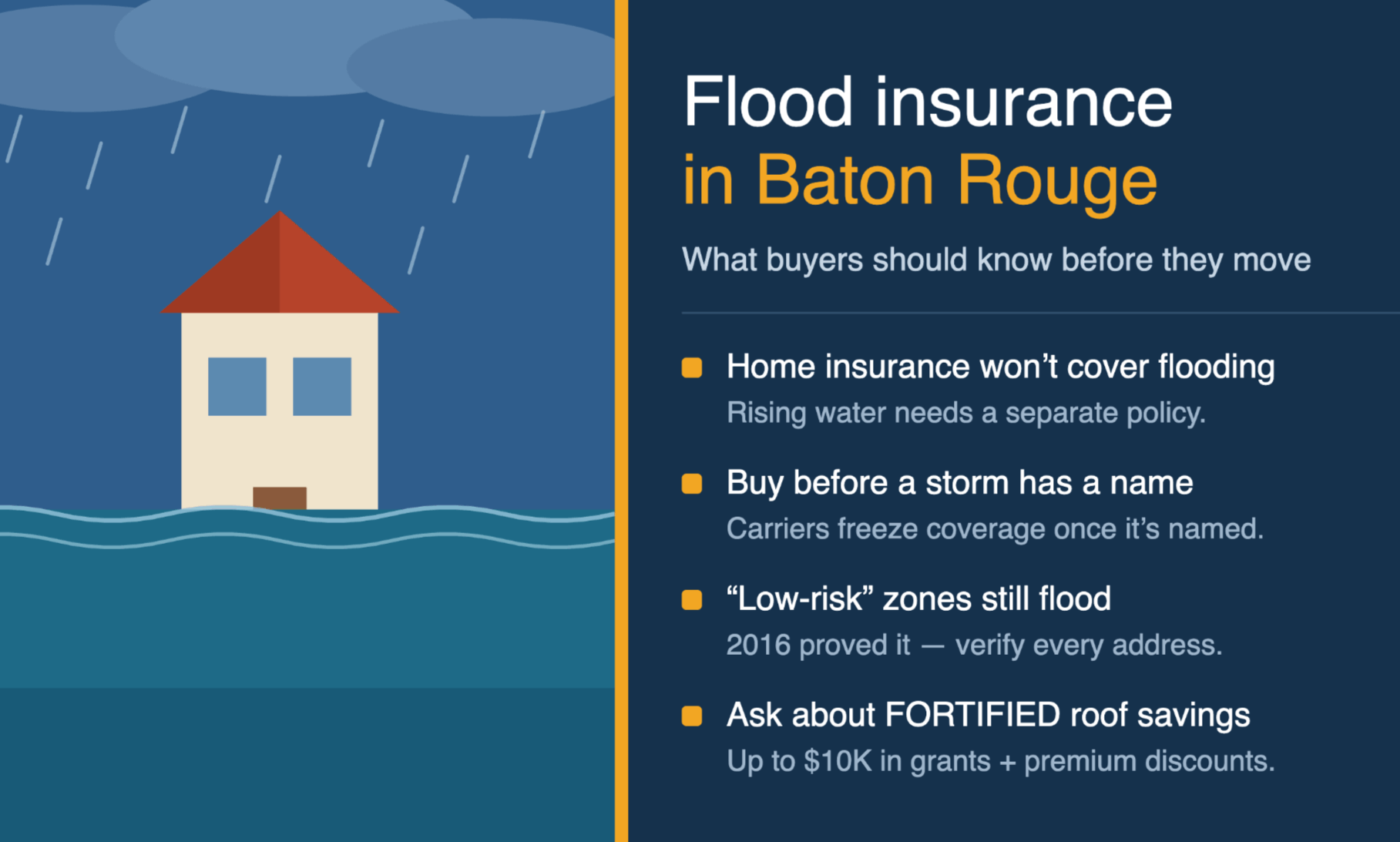

If you remember nothing else from this article, remember this: review and secure your insurance before a storm has a name.

Here's why. Once a named storm enters the Gulf of Mexico, most insurance carriers in Louisiana freeze new policies and changes. That means you typically cannot buy a new flood policy, increase your coverage, or switch carriers until the threat passes. The industry calls it a binding moratorium, and it can stay in place for days. If you wait until the Weather Channel is showing those cone-of-uncertainty maps, you've already missed your window.

On top of that, a brand-new National Flood Insurance Program (NFIP) policy generally carries a 30-day waiting period before it takes effect. Buy a voluntary policy today, and your coverage may not kick in until a month from now.

There's one important exception that matters for relocating buyers: when your lender requires flood insurance and you purchase it in connection with your mortgage closing, that 30-day wait usually doesn't apply — your coverage lines up with your loan. But if you're buying coverage voluntarily, say because you're not in a high-risk zone and your lender isn't requiring it, the 30-day clock is very real. Either way the lesson is the same: don't leave insurance to the last minute, and never assume you can add or change it once a storm is brewing.

“I'm Not in a Flood Zone” Is the Most Expensive Misunderstanding in Louisiana

A lot of buyers relocating here breathe a sigh of relief when they learn their new home isn't in a high-risk flood zone. I understand the instinct, but I want to gently push back on it.

Plenty of homes across the Baton Rouge area including many that flooded in 2016 sit in what FEMA calls Zone X, the moderate-to-low-risk designation that falls outside the high-risk flood zones. That label sounds reassuring, but “low risk” is not “no risk.” Roughly a quarter of flood insurance claims in Louisiana come from properties outside designated high-risk zones. You don't have to live on a bayou to take on water. A clogged drainage canal, an overwhelmed pump station, or ten inches of rain in six hours can put water in a home the maps call low-risk.

The clearest proof is still the August 2016 flood, which damaged tens of thousands of homes across the Greater Baton Rouge region, many of which had never flooded before and sat well outside any high-risk zone. Denham Springs is the textbook case: entire neighborhoods that took on water in 2016 were outside the high-risk zones, which is exactly why so many of those families had no flood coverage. Families who assumed they didn't need flood insurance learned the hard way that the maps don't tell the whole story. So when you're shopping, treat flood risk as something to verify property by property, not something to rule out based on a neighborhood's reputation.

Your Homeowners Policy Does Not Cover Flooding — Full Stop

This is the single biggest misconception I see from out-of-state buyers, so let me be direct: a standard homeowners insurance policy does not cover flood damage. Not storm surge, not drainage overflow, not rising water of any kind. Flood coverage is a separate policy you buy in addition to your homeowners insurance.

The dividing line is wind versus water. If a storm sends a tree through your roof, tears off shingles, or breaks a window, and rain comes in through that wind-created opening that's generally a wind claim under your homeowners policy. But the moment water rises from the ground up, it's classified as flood, and your homeowners policy won't touch it.

There's another wrinkle newcomers rarely expect: the hurricane or named-storm deductible. Many Louisiana homeowners policies carry a separate, percentage-based deductible for named storms — often 2% to 5% of your dwelling coverage, not a flat dollar amount. On a $300,000 home with a 5% hurricane deductible, that's $15,000 out of pocket before your wind coverage even begins. It's worth knowing that number before you buy, not after.

How Flood Insurance Actually Works in Baton Rouge

You generally have two paths to flood coverage: the federal NFIP and private flood insurers.

NFIP policies are government-backed and available almost everywhere, but they cap out at $250,000 for the structure and $100,000 for contents. For many Baton Rouge homes that's plenty; for higher-value homes, it may not be. Private flood insurance has grown a lot in recent years and often offers higher limits and, in some cases, lower prices or fewer exclusions. It's worth getting quotes from both.

What you'll actually pay depends heavily on your specific property. In 2021, FEMA overhauled NFIP pricing with a system called Risk Rating 2.0, which prices each home based on factors like its distance to a water source, the type of flooding it's exposed to, and its elevation not just its zone. When that change rolled out, roughly 80% of NFIP policyholders in Louisiana saw their premiums move. The upshot for you: two homes on the same street can carry very different flood premiums.

As a rough benchmark, most homeowners in East Baton Rouge Parish pay somewhere in the range of $400 to $800 a year for standard NFIP coverage, with homes closer to the Amite or Comite rivers running higher. Please treat that as a starting point, not a quote, your number is specific to the address.

Flood Zones, Elevation Certificates, and What to Check Before You Make an Offer

Because flood costs are so property-specific, the smartest thing a relocating buyer can do is get the flood picture on a home early, ideally before you're emotionally attached, and certainly before your inspection period runs out.

Two terms you'll hear: Base Flood Elevation (BFE), which is FEMA's benchmark for how high floodwater is expected to reach in a given area, and the elevation certificate, a document prepared by a licensed surveyor that shows how your home's lowest floor sits relative to that BFE. A home elevated above the BFE can carry dramatically lower premiums than a similar home sitting below it. For older homes especially, that one document can swing your annual cost by hundreds or even thousands of dollars.

When I work with relocating buyers, I order a flood zone determination early and, when it matters, help you track down or commission an elevation certificate so we know the real number before you commit. The worst time to discover a home's flood premium is after you're already under contract.

A Local Money-Saver Most Newcomers Have Never Heard Of: FORTIFIED Roofs

Here's some genuinely good news, and a program almost no one moving here from out of state knows about. To bring down the wind-and-hurricane side of insurance costs, Louisiana has built what's arguably the most generous roof-resilience incentive structure in the country.

At the center is the Louisiana Fortify Homes Program, which awards grants of up to $10,000 to help homeowners upgrade an existing roof to the IBHS FORTIFIED standard, a stronger roof designed to stand up to hurricane-force wind. The grants are awarded by lottery, with application windows that open and close quickly, and they're limited to primary residences with a homestead exemption. The state keeps investing in it: as of early 2026 there were more than 11,000 FORTIFIED roofs across Louisiana, and in May 2026 lawmakers added another $50 million to fund roughly 5,000 more. Ascension and Livingston parishes are among those covered.

The payoff doesn't stop at the grant. Under a new state rule known as Regulation 136, insurers will be required to give standardized discounts on the hurricane portion of your premium for FORTIFIED-designated homes, benchmarked between 16% and 49% depending on where you are in the state and your roof's certification level — with carriers required to apply them no later than January 1, 2027. There are also state tax incentives of up to $10,000 for qualifying FORTIFIED roof work.

One important clarification so you don't get the wires crossed: FORTIFIED helps with wind and hurricane premiums, not flood. It's a separate benefit from your flood policy. But for a relocating buyer trying to get their arms around the total cost of owning here, it's real money and it's worth asking whether a home you're considering already has a FORTIFIED roof or could qualify.

A Few Louisiana Quirks That Affect Your Flood Picture

Two quick orientation notes for newcomers.

First, Louisiana has parishes, not counties. That's not just a vocabulary difference, your parish handles floodplain permitting and local flood maps, so when you're verifying a property's flood status, the parish is where a lot of the answers live. East Baton Rouge, Ascension, Livingston, and West Baton Rouge each run their own show.

Second, your flood premium isn't set only by your individual property. Communities that participate in FEMA's Community Rating System by exceeding minimum floodplain-management standards can earn NFIP discounts for their residents. It's one more reason two seemingly similar homes in different jurisdictions can price out differently.

The Good News (Because It's Not All Storm Clouds)

I don't want to scare you off — quite the opposite. Louisiana also has some of the lowest property taxes in the country, which softens the overall cost of ownership considerably. Effective property tax rates in East Baton Rouge Parish generally run between about 0.64% and 0.90%, and Livingston Parish is even lower, around 0.41%. For many relocating buyers, the money they save on property taxes here helps offset the insurance line that feels unfamiliar at first. The key is to go in with eyes open and the full picture in front of you of purchase price, taxes, homeowners insurance, flood insurance, and any wind-mitigation savings, so there are no surprises at the closing table.

The Bottom Line for Out-of-State Buyers

Flood insurance in Baton Rouge isn't something to fear, it's something to plan for. Four habits will put you ahead of most buyers who've lived here for years:

- Get your flood and homeowners quotes early, address by address.

- Verify flood risk on the specific property, not the neighborhood's reputation.

- Line your coverage up with your closing date and the NFIP timeline.

- Never wait until a storm has a name to buy or change a policy.

This is exactly the kind of thing I help relocating buyers navigate. As a born-and-raised Baton Rouge native and a relocation specialist, I order flood determinations early, connect you with trusted local insurance agents so your timeline lines up with your move, and make sure you understand the full cost of a home before you fall in love with it. If you're thinking about a move to the Greater Baton Rouge area, I'd love to help you do it the smart way.

Reach out anytime at SharonsellsBR@gmail.com or visit sharonsellsbr.com, and subscribe to my YouTube channel, Sharon Sells Baton Rouge, where I break down what it's really like to live and buy in the Capital Region.

A note: I'm a licensed Louisiana Realtor, not an insurance agent or tax advisor, and this article is general information — not insurance, legal, or tax advice. Flood zones, premiums, programs, and deadlines change, and every property is different. Always confirm specifics with a licensed Louisiana insurance professional, your lender, and the appropriate parish before making decisions. Data referenced here is drawn from sources including FEMA and the National Flood Insurance Program, the Louisiana Department of Insurance, and local reporting.

Sharon Dallalio | Sharon Sells Baton Rouge | LPT Realty | Louisiana License #46644

📲 Call/Text: 225-535-8907

🌐 sharonsellsbr.com

📩 Sharonsellsbr@gmail.com

🏡 LPT Realty | Licensed in Louisiana

340 West Tunnel Blvd, Suite 223, Houma, LA 70360

Categories

Recent Posts

GET MORE INFORMATION